It is a frustrating paradox that many of us know all too well: you work hard, land a promotion, and celebrate a significant raise, yet six months later, your bank account looks exactly the same as it did when you were earning much less. We often assume that the solution to financial struggle is simply “more money,” but for many, a higher salary only acts as a larger bucket for the same leaky holes in their financial foundation. If you find yourself living paycheck to paycheck despite a growing income, the problem likely isn’t your earning potential—it’s the invisible, destructive financial habits keeping you poor by dictating exactly how that money leaves your hands.

In this article, we are going to dive deep into the psychological and practical traps that keep people in a cycle of “comfortable poverty.” We will explore why salary bumps often disappear into thin air and, more importantly, how you can pivot your mindset to finally build the wealth you deserve. Understanding these behaviors is the first step toward breaking the glass ceiling of your personal net worth.

The Illusion of “Making It” and the Reality of Lifestyle Creep

The most common reason people stay broke despite earning more is a phenomenon known as lifestyle inflation. It starts subtly. You get a 10% raise, so you decide it’s finally time to move into a “better” apartment, or perhaps you trade in your reliable sedan for a luxury SUV with a hefty monthly payment. Suddenly, that extra income is entirely spoken for before it even hits your account.

When we treat every increase in income as an invitation to increase our spending, we effectively reset our “zero.” We become trapped in a cycle where our expenses rise in lockstep with our earnings, leaving no room for wealth accumulation. To build true financial freedom, you have to learn to decouple your standard of living from your salary. The goal isn’t to live like a monk, but to ensure that your savings rate grows faster than your spending.

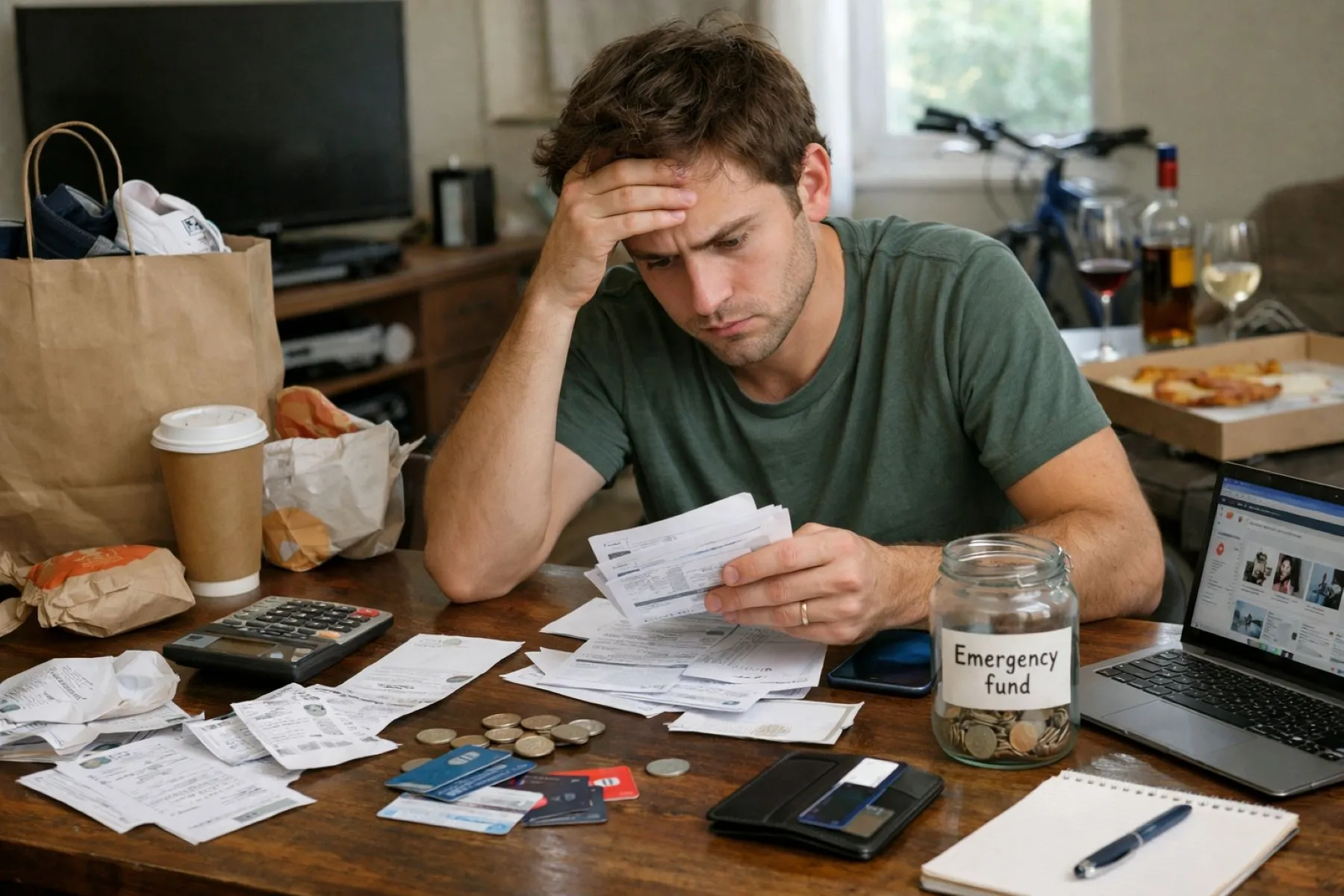

Living on the Edge Without a Safety Net

One of the most dangerous financial habits keeping you poor is the total neglect of emergency savings. When you have a regular salary, it is easy to feel a false sense of security. You assume the paycheck will always be there, so you spend what you have. However, life rarely goes according to plan. A medical emergency, a sudden job loss, or even a major car repair can become a financial catastrophe if you are living on the edge.

Without an emergency fund, you are constantly one bad day away from financial ruin. This lack of a buffer forces you to make desperate decisions, such as taking out high-interest loans or raiding your retirement accounts, which sets your financial progress back by years. An emergency fund isn’t just a pile of cash; it is “peace of mind” insurance that allows you to navigate life’s hiccups without falling back into debt.

The Debt Trap: Relying on High-Interest Credit

We live in a culture that prioritizes instant gratification, often fueled by the plastic in our wallets. Relying on high-interest credit cards to fund a lifestyle you can’t quite afford is like trying to run a marathon with lead weights tied to your ankles. The interest alone can swallow a massive portion of your monthly income, ensuring that a significant chunk of your hard-earned salary goes toward enriching a bank rather than building your own future.

Many people view credit cards as an extension of their income rather than a tool for convenience. When you carry a balance from month to month, you aren’t just paying for that dinner or those shoes; you are paying for them twice or thrice over in interest. Breaking the cycle of poverty requires a radical shift in how you view debt: if you can’t pay for it in cash today, you likely can’t afford it.

Flying Blind: The Danger of Not Tracking Expenses

If I asked you exactly how much you spent on subscriptions, dining out, or “miscellaneous” items last month, could you give me an accurate answer? Most people can’t. Failing to track daily expenses is another one of those subtle financial habits keeping you poor. Small, seemingly insignificant purchases—the $7 latte, the unused gym membership, the premium streaming services—add up to hundreds, if not thousands, of dollars over a year.

When you don’t track your spending, your money simply “disappears.” You end up at the end of the month wondering where it all went. By implementing a simple system to categorize your outflows, you gain the power to identify “leaks” in your budget. It’s not about restricting yourself; it’s about being conscious of where your life energy (represented by your salary) is actually going.

The Cost of Playing It Safe and Ignoring Investments

Many people stay poor because they are afraid of the market or simply don’t understand it. They keep their money in a standard savings account, watching it slowly lose purchasing power due to inflation. While saving is a great first step, it is rarely enough to build true wealth. To move from “stable” to “wealthy,” your money needs to work for you.

Ignoring long-term investment opportunities, such as a 401(k), index funds, or real estate, is a habit that costs you millions over a lifetime. The magic of compound interest only works if you give it time. By delaying your entry into the world of investing, you are essentially trading your future freedom for present-day comfort. Even small, consistent contributions to an investment account can grow into a substantial nest egg, but you have to be willing to take that first step.

The Social Pressure to “Look” Wealthy

We are social creatures, and the urge to keep up with the Joneses—or the influencers on our Instagram feeds—is incredibly powerful. Impulsive social pressure often leads us to spend money we don’t have to impress people we don’t even like. Whether it’s attending every expensive brunch, buying the latest smartphone, or wearing designer labels, the cost of “performing” wealth is often the very thing that prevents us from actually achieving it.

True wealth is quiet; it’s the money you don’t spend on flashy things. When you prioritize social validation over financial security, you are essentially letting other people’s expectations dictate your bank balance. Learning to say “no” to social outings that don’t fit your budget is a superpower. It’s a sign of maturity and a clear indicator that you value your future more than a temporary ego boost.

Wandering Aimlessly Without Financial Goals

Finally, the most pervasive habit that keeps people stuck is a lack of clarity. If you don’t have clear, written monthly and yearly financial goals, your money will naturally flow toward the path of least resistance: consumption. Without a “why,” it is almost impossible to maintain the discipline needed to save and invest.

Are you saving for a house? Are you aiming to be debt-free by 35? Do you want to retire early? When you have a concrete goal, every dollar you earn becomes a soldier in a mission to achieve that goal. Without a plan, your salary is just a temporary resource that gets used up and forgotten. Setting goals gives your financial life a sense of purpose and direction.

Practical Steps to Reclaim Your Financial Future

Breaking the financial habits keeping you poor doesn’t happen overnight, but you can start today with a few intentional shifts in your daily routine:

-

Implement the 24-Hour Rule: Before any non-essential purchase over $50, wait 24 hours. Most of the time, the “must-have” feeling will fade.

-

Automate Your Savings: Treat your savings like a bill that must be paid. Set up an automatic transfer to your savings or investment account the day your paycheck arrives.

-

Audit Your Subscriptions: Look at your bank statement and cancel anything you haven’t used in the last 30 days. You’d be surprised how much is hiding there.

-

Adopt a “Value-Based” Spending Mindset: Spend lavishly on the things that truly bring you joy and improve your life, but cut costs mercilessly on the things that don’t.

Choosing Prosperity Over Pretense

Financial struggle is rarely a matter of bad luck; more often, it is a collection of small, daily choices that compound over time. The good news is that habits can be rewritten. By identifying these destructive patterns, you have already taken the most difficult step: awareness.

True financial freedom isn’t about how much you earn; it’s about how much you keep and how hard that money works for you. It requires the courage to live differently than the crowd and the discipline to prioritize your long-term dreams over short-term impulses. You have the power to break the cycle of poverty and turn your regular salary into a tool for lasting wealth.