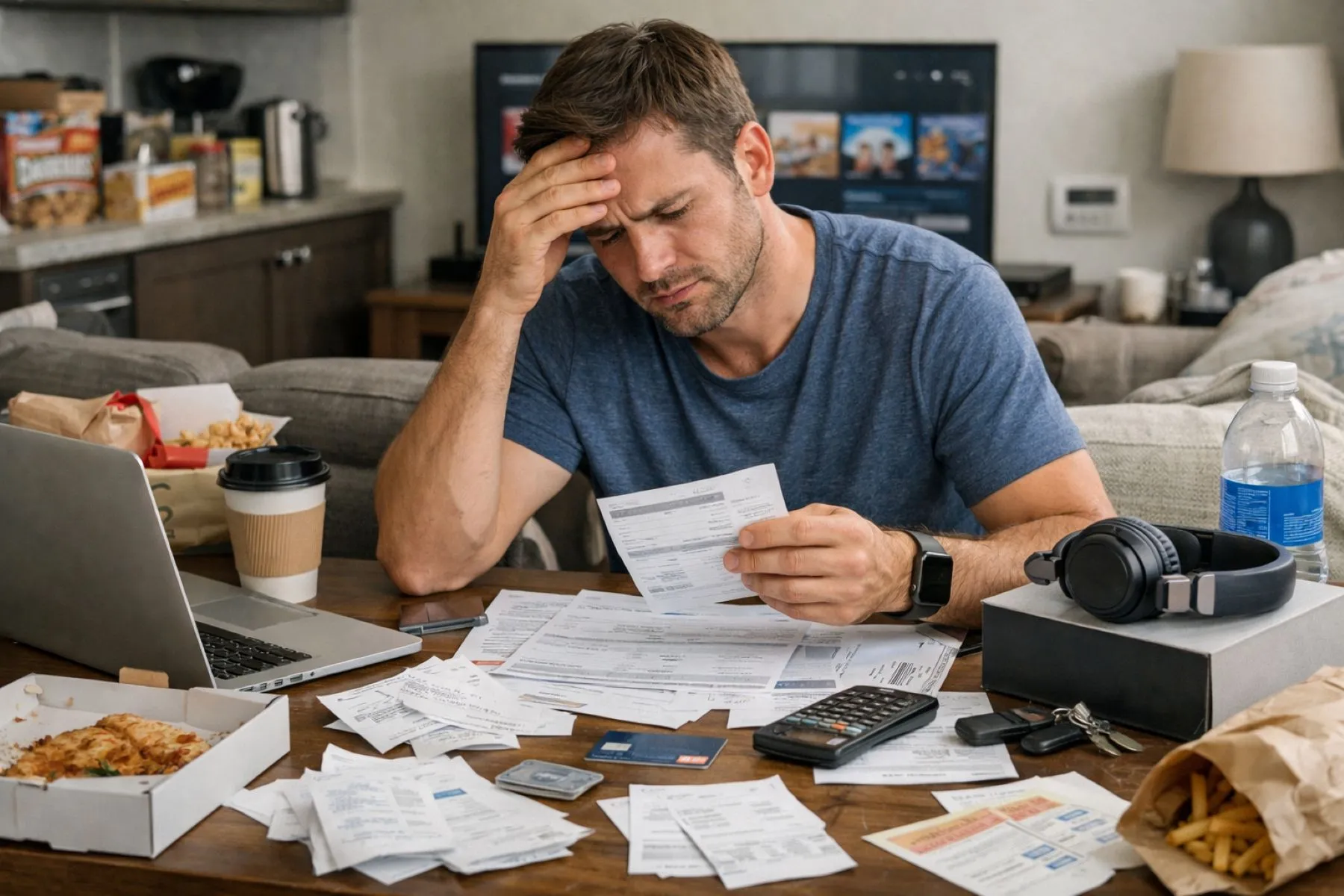

We often think of financial ruin as a singular, catastrophic event—a massive stock market crash, a failed business venture, or a sudden job loss. While those events are certainly impactful, the reality for most of us is that wealth doesn’t usually disappear in one giant leap; it leaks out in tiny, almost invisible drops. These are the “silent” personal finance mistakes we make while standing in the checkout line, scrolling through our phones, or simply going about our morning routines. They seem harmless because they involve small amounts of money, but over time, they form a heavy anchor that keeps our savings accounts from ever truly taking flight.

Understanding these habits isn’t about embracing a life of deprivation or counting every single penny until you’re miserable. It’s about awareness. Most of us are bleeding cash simply because we’ve automated our lives to the point of financial unconsciousness. By identifying these subtle drains, you can plug the holes in your “leaky bucket” and redirect that capital toward goals that actually matter. If you’ve ever looked at your bank balance on the 20th of the month and wondered where it all went, this guide is for you.

The Invisible Leak of Small Cash and Subscriptions

One of the most common personal finance mistakes is losing track of money through the “latte factor” magnified by a hundred. It’s not just the coffee; it’s the spontaneous snack at the gas station, the $2 parking fee we didn’t plan for, or the cash we hand over for small convenience items. Because these transactions are small, they often bypass our mental “budgeting filter.” We treat them as if they don’t count, but at the end of the year, these neglected daily expenses can easily total thousands of dollars.

The digital-age equivalent of this leak is the explosion of monthly subscription services. From streaming platforms to “box-of-the-month” clubs, we live in a subscription economy. The danger here is the “set it and forget it” mentality. Many of us are paying for premium versions of apps we no longer use or multiple services with overlapping content. These $9.99 charges are designed to stay under your radar, acting as a permanent drain on your monthly cash flow.

The Branding Trap and Other Common Personal Finance Mistakes

Marketing is a powerful force, and one of the most effective traps we fall for is the psychological lure of premium brands. Whether it’s household cleaners or pantry staples, we often pay a 30% to 50% markup just for a familiar logo. In many cases, the generic version contains the exact same ingredients. By defaulting to the “name brand” out of habit, you are essentially paying a tax on your own lack of curiosity.

Similarly, we often pay a high price for a few minutes of saved time. Frequent out-of-network ATM fees are perhaps the most egregious example. Paying $3 to access your own money is a 100% loss with zero return. The same applies to food delivery services. Between delivery fees and inflated menu prices, a $15 meal can easily turn into a $30 expense. When this becomes a habit, you are trading long-term financial security for short-term convenience.

The Psychology of the Modern Marketplace

Retailers are experts at “choice architecture,” designed specifically to make you spend money you hadn’t planned to. Have you ever noticed how the checkout lane is lined with magazines and snacks? These are strategic impulse displays targeting the “decision fatigue” you feel after navigating the aisles. By the time you reach the register, your willpower is low, making you the perfect target for a $5 purchase you don’t need.

This lack of intentionality often extends to the grocery store as a whole. Failing to compare prices or unit costs is a major oversight. A larger package isn’t always a better deal, and prices can fluctuate wildly. Without a fixed budget and a shopping list, you aren’t just buying food; you’re participating in a sensory experience designed to maximize the store’s profit. Shopping without a plan is essentially an invitation for the store to tell you how much you should spend.

Avoiding Personal Finance Mistakes in Household and Digital Drains

Sometimes, the money is leaving your house through the literal walls. Overlooking hidden utility waste is a classic financial pitfall. This includes “vampire power” from electronics that stay plugged in but unused, or water heaters set to a temperature higher than necessary. Individually, these are small costs, but they add up to a significantly higher cost of living over the course of a decade.

In the digital realm, we often forget to track receipts or monitor credit card interest rates. In an era of autopay, it’s easy to ignore the fact that your interest rate might have climbed. Furthermore, many consumers fall for the trap of extended product warranties. Statistically, most electronics are either reliable enough to last or will fail within the standard manufacturer’s period. Buying that extra “peace of mind” is usually just a high-margin profit center for the retailer, not a smart move for your wallet.

Maintenance vs. Repair: The Long-Term Cost

One of the most expensive personal finance mistakes you can make is trying to save money by skipping scheduled preventive maintenance. This applies to your car, your home, and even your health. Forgetting an oil change or ignoring a small leak might save you $100 today, but it sets the stage for a $5,000 repair bill next year. Financial health requires a shift from a reactive mindset to a proactive one. Maintenance is an investment; repair is a penalty.

This reactive mindset is also seen in how we use credit. Using credit cards for non-essential goods—items that lose value the moment you buy them—is a recipe for long-term struggle. When you carry a balance on a luxury item, you aren’t just paying for the item; you’re paying for the item plus 20% interest. This makes everything you buy more expensive than the price tag suggests, trapping you in a cycle where you are constantly paying for your past instead of investing in your future.

Practical Steps to Reclaim Your Income

The journey to financial clarity doesn’t require a radical lifestyle overhaul. Instead, it starts with a few tactical shifts that build momentum:

-

The 48-Hour Rule: For any non-essential purchase over $30, wait 48 hours to let the impulse fade.

-

Audit Your Digital Life: Once a month, review every recurring charge. If you haven’t used it in 30 days, cancel it.

-

The “Unit Price” Habit: Look at the small print on the shelf tag to see the price per ounce. This is the only way to find the real deal.

-

Automate Your Savings: Set up a system where a portion of your paycheck goes directly into a high-yield savings account before you ever see it.

-

Embrace Generic: Challenge yourself to buy the store brand for five common items to see if you can actually tell the difference.

Securing Your Financial Future

Eliminating these personal finance mistakes isn’t about being “cheap”—it’s about being intentional. Every dollar you stop wasting on a hidden fee, a branded cereal, or an unused subscription is a dollar that can work for you. It can be invested, used to pay down high-interest debt, or saved for a goal that truly brings you joy.

True wealth is built in the margins. By cleaning up these small, messy habits, you regain control over your narrative. You stop being a passive participant in the consumer economy and start being the architect of your own financial freedom. Remember, a small leak can sink a great ship, but once that leak is plugged, you have the power to sail wherever you choose.