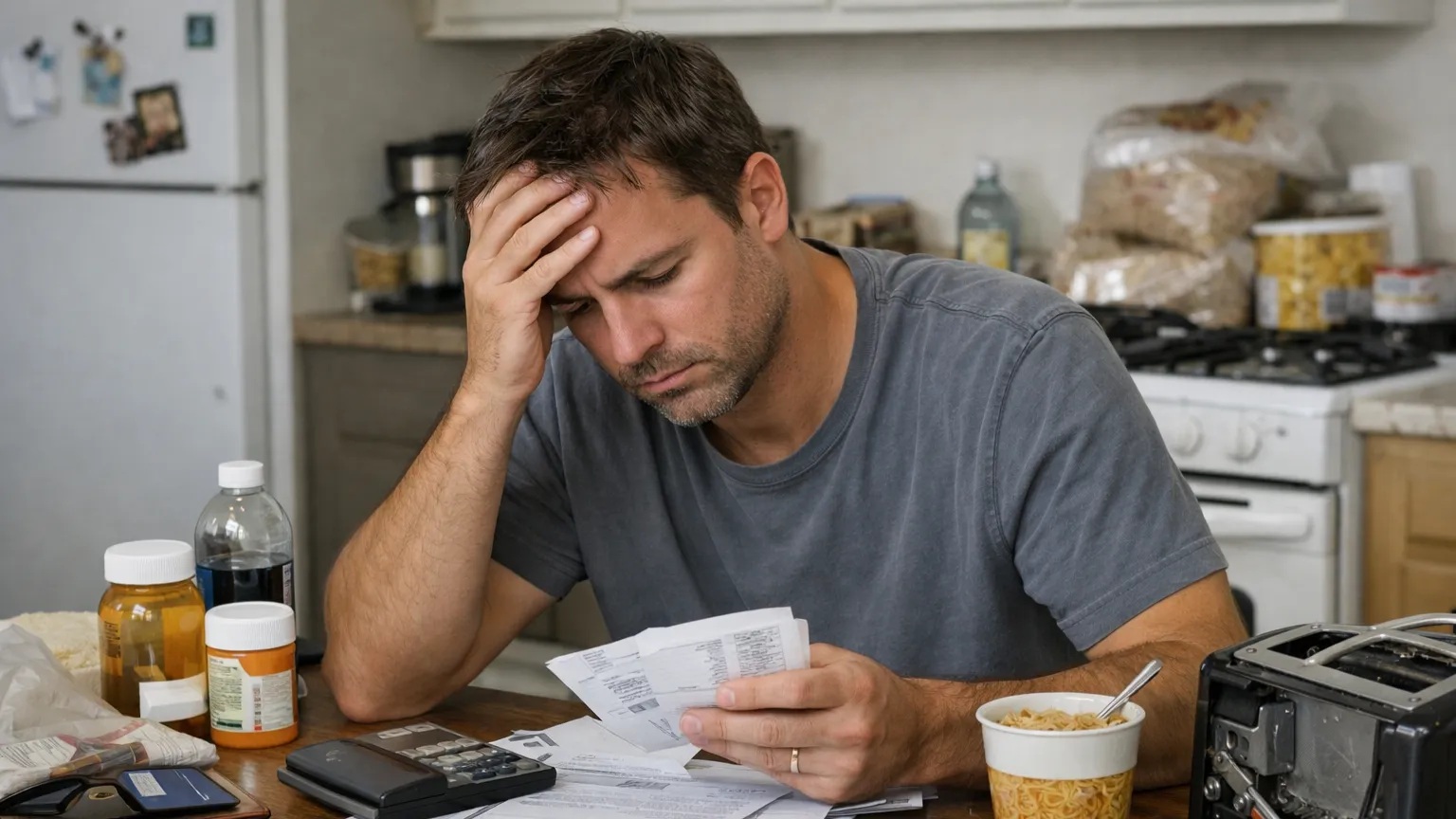

We have all been there—staring at a bank statement that feels a little too lean, feeling that sudden jolt of adrenaline that demands we “cut back everything.” It’s a natural survival instinct. In an effort to regain control, we start slashing subscriptions, opting for the cheapest possible groceries, and swearing off every social invitation for the next six months. On paper, it looks like a masterstroke of discipline. In reality, however, many of these drastic measures are actually financial mismanagement mistakes in disguise.

The journey to financial stability is rarely about who can suffer the most; it is about who can manage their resources most efficiently. When we approach expense reduction with a “scorched earth” mentality, we often trade our long-term security for short-term liquidity. This article explores how well-intentioned savings can backfire, the psychological traps that lead us astray, and how you can trim your budget without accidentally pulling the rug out from under your own feet. By understanding these pitfalls, you can build a personal economy that isn’t just “cheap,” but truly resilient.

Understanding Common Psychological Pitfalls

Before we look at the numbers, we have to look at the mind. Most financial errors start as psychological blind spots. One of the most pervasive is the underestimation of small, daily transactions. It’s easy to focus on the big $500 car payment, but we often ignore the $5 convenience store snacks or the $10 digital “micro-transactions” that bleed a budget dry through sheer frequency. Because these amounts don’t feel “heavy,” they bypass our internal alarm systems.

Then there is the complex world of emotional spending triggers. We often cut costs in areas that provide us joy, only to find ourselves “revenge spending” later because we feel deprived. If you cut out your morning coffee but end up buying a $100 pair of shoes because you had a stressful week and “deserved a treat,” the math simply doesn’t work. True cost-cutting requires an honest assessment of why we spend, not just what we spend.

Perhaps the most dangerous psychological trap is the habit of sacrificing quality for cheapness. There is a profound difference between being frugal and being cheap. Frugality is about getting the best value for your money; being cheap is simply paying the lowest price possible. When we prioritize the sticker price over the utility and longevity of an item, we are almost always guaranteeing a secondary expense down the road.

Common Financial Mismanagement Mistakes in Reducing Expenses

When people enter a “savings panic,” they often look for the largest monthly bills to eliminate. Frequently, insurance coverage is the first on the chopping block. It feels like “free money” because you aren’t using it daily. However, reducing or eliminating essential insurance—be it health, auto, or home—is one of the most significant financial mismanagement mistakes you can make. One unlucky incident can transform a $100 monthly saving into a $50,000 catastrophic debt.

Similarly, many try to save by skipping routine preventative maintenance. Whether it’s delaying an oil change for your car, ignoring a small leak in the roof, or skipping a dental cleaning, the logic is the same: “I’ll save this money now and deal with the problem later.” Unfortunately, the “later” version of that problem is always more expensive. Maintenance is an investment in preventing failure; skipping it is just taking out a high-interest loan against your future.

We also see this in the “bulk-buying” trap. Buying in bulk is only a saving if you actually need and use the items before they expire or become irrelevant. Filling a pantry with items you don’t particularly like just because they were on sale isn’t saving—it’s cluttering. This extends to our physical health as well. Cutting back on nutritious food or gym memberships might lower your monthly outgoings, but the resulting decline in energy and the increased risk of medical issues create a financial burden that no coupon can fix.

Why Radical Budgeting Often Fails

Radical budgeting is the financial equivalent of a crash diet. It might produce results for the first two weeks, but it is rarely sustainable. The primary reason is mental fatigue. Constant self-denial requires an immense amount of willpower, and willpower is a finite resource. When you are constantly weighing every cent, you eventually experience “decision fatigue,” which leads to a total collapse of discipline and a massive rebound spending spree.

Furthermore, these extreme budgets often lack realistic emergency buffers. If your budget is so tight that a flat tire or a broken microwave throws your entire month into chaos, you haven’t created a plan; you’ve created a fragile glass house. A budget must breathe. Without a “miscellaneous” or “emergency” category, you aren’t actually managing your money—you’re just hoping that nothing goes wrong.

We must also consider the invisible hand of inflation. A radical budget created three years ago likely won’t work today. If you fail to account for the rising costs of basic goods and services, your “fixed” budget will eventually become a deficit. Staying rigid in a shifting economy is a recipe for destabilization.

Hidden Costs and Financial Mismanagement Mistakes

The “buy it cheap, buy it twice” adage exists for a reason. Choosing low-quality goods often leads to shorter product life cycles. A $20 pair of shoes that lasts four months is significantly more expensive than an $80 pair that lasts three years. When you are constantly replacing items, you are stuck in a cycle of “poverty charges”—paying more over time because you cannot afford the upfront cost of quality.

Beyond replacement costs, low-quality items often have poor energy efficiency ratings. This is particularly true for appliances and electronics. That “bargain” air conditioner or refrigerator might save you $100 at the store, but it could easily add $20 to your electricity bill every single month. Over the life of the product, the “savings” evaporate into the pockets of the utility company.

There is also a hidden environmental and personal cost. Cheap goods often come with a higher waste impact, contributing to a throwaway culture that eventually affects global resource prices. Moreover, using tools or goods that break easily or perform poorly causes frustration and reduces your overall quality of life. Financial stability should enhance your life, not make every daily task more difficult.

How to Cut Costs Without Risking Stability

If the goal is to reduce expenses safely, the first step is an audit of recurring digital subscriptions. In the age of “subscription creep,” many of us are paying for streaming services, apps, and memberships we haven’t touched in months. This is low-hanging fruit—it reduces your outgoings without changing your lifestyle at all.

Next, try negotiating rather than canceling. Many service providers (internet, insurance, cell phone) have retention departments authorized to give discounts to keep customers. A twenty-minute phone call can often result in a 10% to 20% reduction in your bill without any loss of service. This is a far more effective strategy than cutting out essential services entirely.

Another powerful tool is the “30-day waiting rule” for non-essential purchases. If you see something you want, wait a month. If the desire is still there after thirty days, it’s likely a considered purchase rather than an impulse. Often, you’ll find that the “need” was just a passing whim. Simultaneously, ensure you are automating your savings. If the money leaves your account the moment you get paid, you are less likely to miss it, and you ensure your future is paid for before your present is spent.

Distinguishing Needs from Temporary Desires

At the heart of any stable economy is the ability to categorize survival versus lifestyle. Survival needs are non-negotiable: housing, basic nutrition, essential transport, and healthcare. Lifestyle expenses are everything else. When things get tight, you must be able to distinguish between “I need a car to get to work” and “I need this specific car to feel successful.”

A helpful metric is the “cost-per-use” analysis. A $1,000 laptop that you use for eight hours every day for four years has a remarkably low cost-per-use. A $50 dress you wear once to a wedding has a very high cost-per-use. High-use items deserve a higher budget allocation; low-use items are where the real cuts should happen.

Finally, review your historical spending patterns to set clear financial boundaries. Look back at the last six months and see where the “leaks” are. Once you identify them, create boundaries that protect your peace of mind. Financial stability isn’t about having the most money; it’s about having the most control. When you stop making emotional “cheap” decisions and start making logical “value” decisions, your personal economy will begin to stabilize and grow.

Building a Resilient Financial Future

The path to a secure personal economy is paved with intentionality, not deprivation. When we fall into the trap of financial mismanagement mistakes—cutting the wrong corners and ignoring the long-term impact of our choices—we don’t actually save money; we just postpone the bill. By focusing on value, maintaining your assets, and being honest about your emotional triggers, you create a budget that supports your life rather than restricting it.

Remember, the goal of reducing expenses is to give yourself more freedom, not less. True wealth is built through consistent, sustainable habits that can survive both the good times and the bad.

No Response