Managing money often feels like a constant tug-of-war between the person you are today and the person you want to become. We are frequently told that “budgeting” is an act of restriction—a clinical exercise in saying “no” to the things we enjoy. However, true strategic personal budgeting isn’t about deprivation; it is the art of intentionality. It is a financial roadmap that ensures your hard-earned resources are flowing toward the experiences and items that actually move the needle on your happiness. By shifting our perspective from “saving for a rainy day” to “allocating for a better life,” we can transform our finances from a source of stress into a powerful tool for lifestyle design.

In this guide, we will explore how to stop the “leaks” in your bank account and redirect those funds toward a life of higher quality. Whether you are looking to climb out of debt or simply want to ensure your six-figure salary actually buys you the freedom you crave, understanding the mechanics of strategic allocation is the first step toward a richer existence—both literally and figuratively.

Identifying Your High-Impact Lifestyle Values

Before you even touch a spreadsheet, you have to look in the mirror. Most people fail at fiscal management because they try to follow someone else’s rules. They cut out the $5 latte because a “finance guru” told them to, even though that morning coffee is the highlight of their workday. Effective strategic personal budgeting begins with identifying your high-impact lifestyle values. These are the specific areas of spending that provide you with the most significant return on investment in terms of joy, health, or productivity.

For some, it’s travel; for others, it’s high-quality organic food or a gym membership that actually gets used. When you identify these pillars, you give yourself permission to spend guilt-free in those categories. The trade-off, of course, is being ruthlessly aggressive in cutting costs in areas that don’t matter to you. If you don’t care about cars, driving a reliable ten-year-old sedan allows you to divert thousands of dollars toward your actual passions. This isn’t about being cheap; it’s about being a specialist in your own happiness.

The Power of Automated Wealth Distribution

Decision fatigue is the silent killer of financial goals. Every time you have to manually move money into a savings account or pay a bill, you are forced to exercise willpower. Eventually, willpower runs out. The most successful practitioners of strategic personal budgeting remove the human element as much as possible by implementing automated wealth distribution. This is the “set it and forget it” philosophy applied to your paycheck.

Ideally, your income should be split the moment it hits your account. Direct deposits should be channeled into separate “buckets”: one for fixed necessities, one for long-term investments, one for an emergency fund, and one for guilt-free discretionary spending. By automating these movements, you ensure that your future self is taken care of before you even have the chance to see the money in your primary spending account. This creates a psychological ceiling on your spending that feels natural rather than forced.

Eliminating the “Ghost” Expenses in Your Life

We live in a subscription economy, and it is designed to bleed us dry $9.99 at a time. One of the most effective ways to reclaim your cash flow is to perform a surgical strike on hidden recurring expenses. These “ghost” expenses—streaming services you no longer watch, gym memberships from three New Year’s resolutions ago, or premium app features you forgot you signed up for—act like tiny holes in a bucket. Individually, they seem harmless; collectively, they can drain hundreds of dollars a month.

A strategic audit of your bank statements from the last ninety days usually reveals at least three or four services that no longer serve your high-impact values. Canceling these isn’t just about the money; it’s about reclaiming mental bandwidth. Every recurring charge is a tiny tether to a service you have to manage. Cutting them loose simplifies your financial life and boosts your monthly surplus without changing your daily habits one bit.

Choosing Quality Over Acquisition Volume

There is a pervasive myth that having more things leads to a better life. In reality, a high volume of low-quality acquisitions leads to “clutter stress” and a cycle of constant replacement. A core tenet of strategic personal budgeting is the “buy once, cry once” mentality. This means prioritizing the purchase of high-quality items that last longer and perform better, even if the upfront cost is significantly higher.

Consider a professional-grade kitchen knife versus a cheap set from a big-box store. The professional knife makes cooking safer and more enjoyable, and it can last a lifetime with proper care. The cheap set will dull, break, and end up in a landfill within two years. When you focus on quality over volume, you naturally own fewer things, but the things you do own are exceptional. This shift reduces the long-term cost of ownership and elevates the aesthetic and functional quality of your daily life.

Leveraging the Psychology of Spending Triggers

Our brains are hardwired to respond to marketing, discounts, and the “thrill of the hunt.” To manage your money effectively, you must understand your own psychological spending triggers. Are you a “stress shopper”? Do you spend more when you are scrolling through social media at midnight? Or perhaps you fall for the “it’s on sale” trap, buying things you never wanted just because they are 40% off.

One of the best ways to combat these triggers is the 72-hour rule. For any non-essential purchase over a certain dollar amount, force yourself to wait three full days. Usually, the dopamine hit of the “idea” of the purchase fades, and you realize you don’t actually need the item. By inserting a gap between the impulse and the action, you regain control over your resources and ensure that your spending is aligned with your long-term blueprint rather than a fleeting emotion.

Practical Steps for Your Budgeting Audit

If you’re ready to turn these concepts into a reality, you don’t need a complex software suite. You just need a little bit of honesty and a few hours of focused time. Here is how to execute an audit of your monthly discretionary cash flow:

-

Categorize by Emotion: Look at your last month of spending. Instead of just labeling things as “Food” or “Entertainment,” label them as “Necessary,” “Joy-Giving,” or “Mindless.” The “Mindless” category is where your biggest wins are hidden.

-

The “Price-Per-Use” Calculation: Before buying something new, estimate how many times you will actually use it. A $200 jacket you wear 100 times costs $2 per wear. A $50 dress you wear once for a wedding costs $50 per wear. The $200 jacket is the more strategic purchase.

-

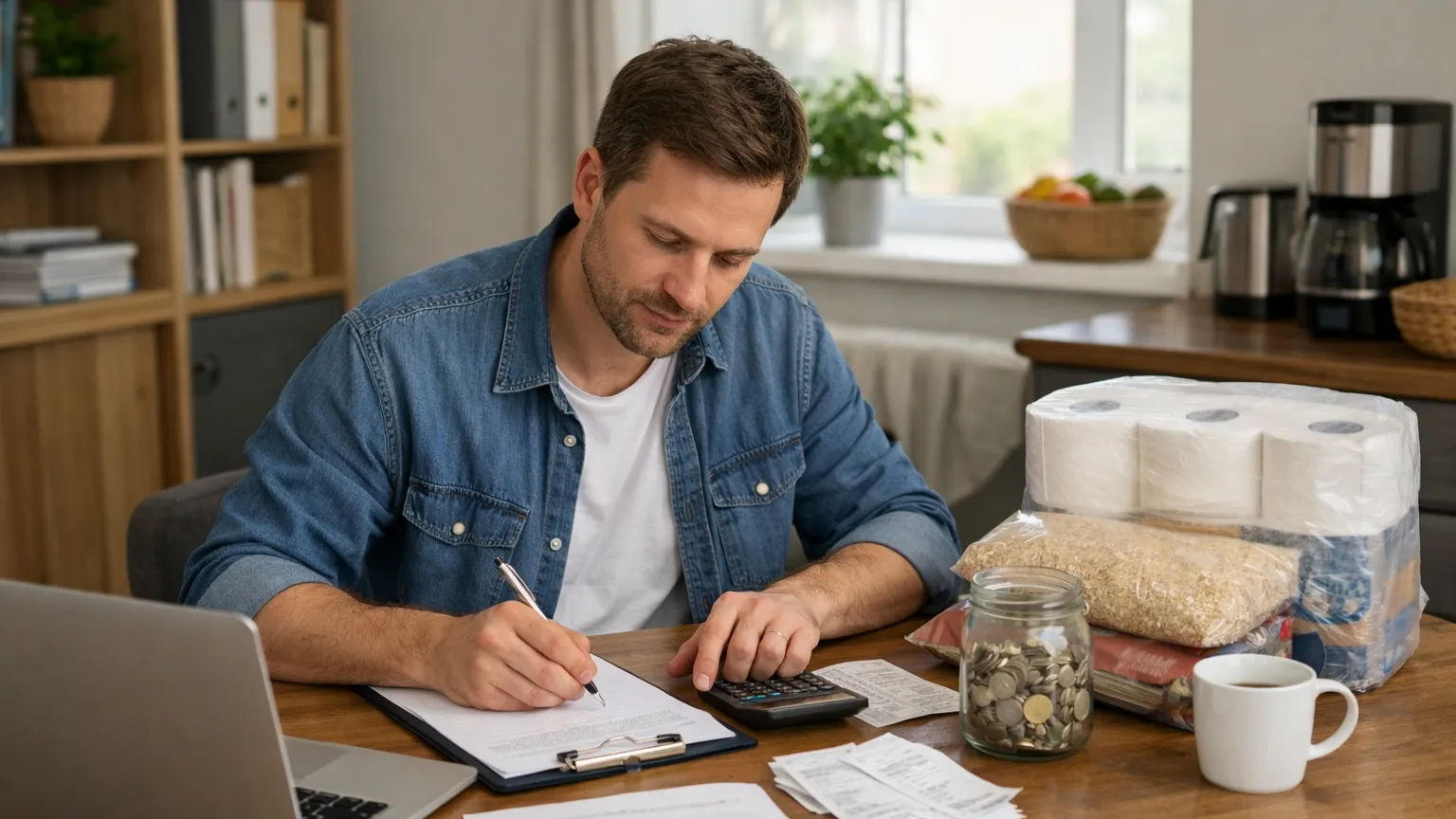

Strategic Bulk Purchasing: Identify non-perishable items you use daily—toiletries, dry goods, office supplies—and buy them in bulk. This reduces your “per-unit” cost and prevents those frequent, expensive “quick trips” to the store where you inevitably buy five things you didn’t need.

-

Negotiate Fixed Costs: Many “fixed” expenses aren’t actually fixed. Once a year, call your internet provider, insurance agent, or cell phone carrier. Often, a fifteen-minute conversation can shave $20–$50 off your monthly bill just by asking for a current promotion or a loyalty discount.

Designing a Life of Abundance

At the end of the day, strategic personal budgeting is about freedom. It is the freedom to say “yes” to a last-minute trip because you’ve eliminated the ghost expenses that were eating your travel fund. It is the peace of mind that comes from knowing your bills are paid automatically, allowing you to focus your creative energy on your career or your family.

When you align your spending with your values, money stops being a source of anxiety and starts being a reflection of your priorities. You aren’t just managing numbers on a screen; you are designing a life. Start by picking one “ghost expense” to cancel today and one “high-impact value” to invest in tomorrow.