The “middle class” is often described as the backbone of the economy, yet for many, it feels more like a gilded cage. You earn a decent salary, live in a nice neighborhood, and can afford the occasional vacation, but at the end of every month, your bank balance looks suspiciously low. This stagnation is rarely the result of one catastrophic mistake; instead, it stems from common middle-class financial habits—the quiet, daily accumulation of subtle behaviors that prevent wealth from actually sticking to you.

Understanding why the climb from “comfortable” to “financially free” is so difficult requires looking beyond the numbers on your paycheck. It’s about identifying the invisible anchors—those toxic patterns we’ve been conditioned to view as normal—that keep us tethered to a survival treadmill. By recognizing these habits, you can stop merely managing your monthly expenses and start engineering your prosperity.

The Comfort Trap of Earned Income

One of the most dangerous myths we’re taught is that a high salary is the same thing as wealth. It isn’t. Relying solely on earned income—trading your hours for dollars—is the ultimate glass ceiling. When your financial survival depends entirely on your physical presence and productivity, you are always one burnout or one corporate restructuring away from a crisis.

The middle class often falls into the trap of seeking a “better job” to solve financial woes, while the truly wealthy focus on acquiring assets that work when they don’t. Until you decouple your income from your time, you aren’t building wealth; you’re just maintaining a high-end subscription to your own life.

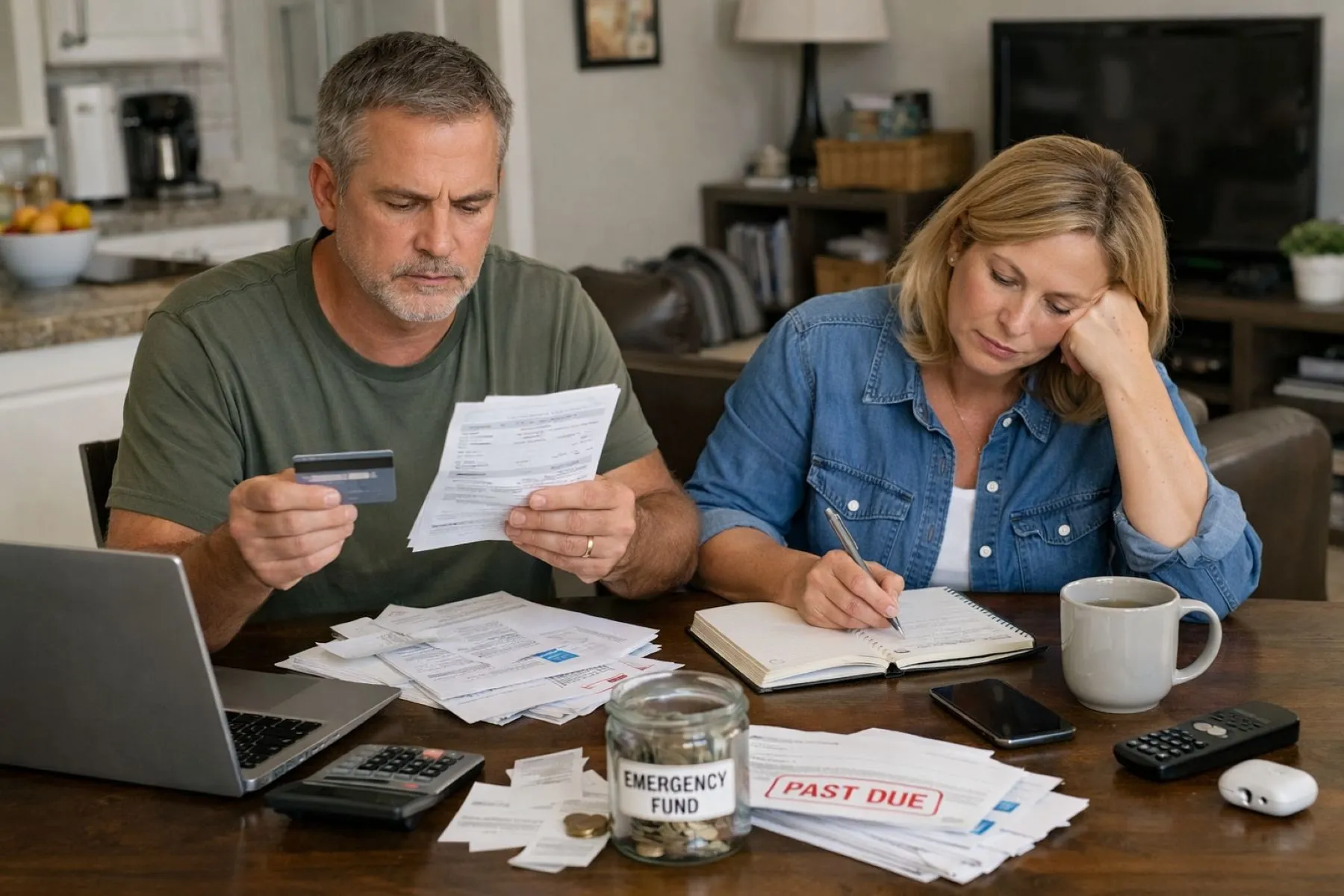

The Debt Cycle and Budgeting Blind Spots

High-interest consumer debt is perhaps the most efficient wealth-killer ever devised. Many of us treat credit card balances as a “tomorrow problem.” However, paying $15\%$ or $20\%$ interest on a dinner you ate three months ago is mathematically sabotaging your future. This is often compounded by inconsistent budgeting. Without a clear map of where every dollar goes, money tends to evaporate. A “rough idea” of your spending is usually an invitation for lifestyle creep to take over, leaving you wondering where your raises went.

12 Toxic Middle-Class Financial Habits That Stagnate Your Wealth

-

Relying Solely on a Single Paycheck

The “active income” trap is real. If you don’t have dividends, rental income, or a side business, your growth is linear. Breaking into the next tier of wealth requires exponential growth through diversified income streams.

-

Feeding the High-Interest Monster

Neglecting high-interest debt is like trying to fill a bucket with a hole in the bottom. Before you can invest, you must stop the bleeding. The interest you pay to banks is wealth that could have been compounding in your own accounts.

-

The “Vibe-Based” Budget

Practicing inconsistent monthly budgeting creates a lack of accountability. Precision in tracking is what separates those who grow wealth from those who just survive.

-

Immediate Lifestyle Inflation

Every time you get a promotion, do you upgrade your car? This is a classic example of middle-class financial habits where expenses rise in lockstep with income, keeping your net worth flat.

-

Living on the Edge of an Emergency

Maintaining insufficient cash reserves forces you to rely on credit cards during a crisis. A solid cash cushion is the foundation of financial peace of mind.

-

Playing It Too Safe with Investments

Avoiding long-term equity investments because of “market volatility” is a hidden risk. Cash in a standard savings account often loses purchasing power to inflation over time.

-

The Manual Savings Struggle

If you wait until the end of the month to see what’s left to save, the answer is usually “nothing.” Failing to automate your savings means you are constantly negotiating with your own willpower.

-

The New Car Fever

Purchasing brand-new vehicles—depreciating assets—is a major pitfall. Wealthy individuals tend to buy assets that appreciate, while the middle class buys things that lose value the moment they leave the lot.

-

Subscription Hemorrhaging

In the digital age, we are “nickeled and dimed” to death. Overlooking hidden costs for streaming services and apps can quietly drain thousands of dollars over a few years.

-

Aimless Financial Wandering

Lacking specific milestones makes it impossible to measure progress. Without a target (e.g., “Invest $1k a month”), you’ll hit nothing every single time.

-

Emotional Impulse Buying

Making emotional buying decisions bypasses the logical brain. If it wasn’t a “yes” yesterday, it shouldn’t be a “yes” today just because you’re stressed.

-

Ignoring the Tax Man

Disregarding professional tax planning is a costly mistake. Utilizing the right accounts and deductions can save you a fortune, leaving more capital to reinvest.

Practical Steps to Overcome Common Middle-Class Financial Habits

Breaking these habits requires a shift in identity from a “consumer” to an “owner.” Start by automating your financial life. Set up your accounts so that a portion of your paycheck disappears into an investment account before you even see it.

Next, conduct a lifestyle audit. Identify the “leaks” in your last three months of spending. Use that recovered cash to aggressively kill any debt with an interest rate higher than $7\%$. Once the debt is gone, redirect those same payments into the stock market or other appreciating assets. Finally, educate yourself on tax-advantaged accounts like a 401(k) or IRA; these are the tools that allow your money to grow without a massive tax bite.

Closing the Gap

The transition from the middle class to true financial independence isn’t about luck; it’s about the discipline to reject “normal” behaviors. Most people remain stuck because they do what “most people” do. By auditing your daily actions and eliminating these toxic middle-class financial habits, you aren’t just saving money—you are buying back your future time.

Wealth is built one intentional decision at a time. Reflect on which of these twelve habits is currently holding the most power over your bank account. Acknowledge it without guilt, and then commit to a different path today.